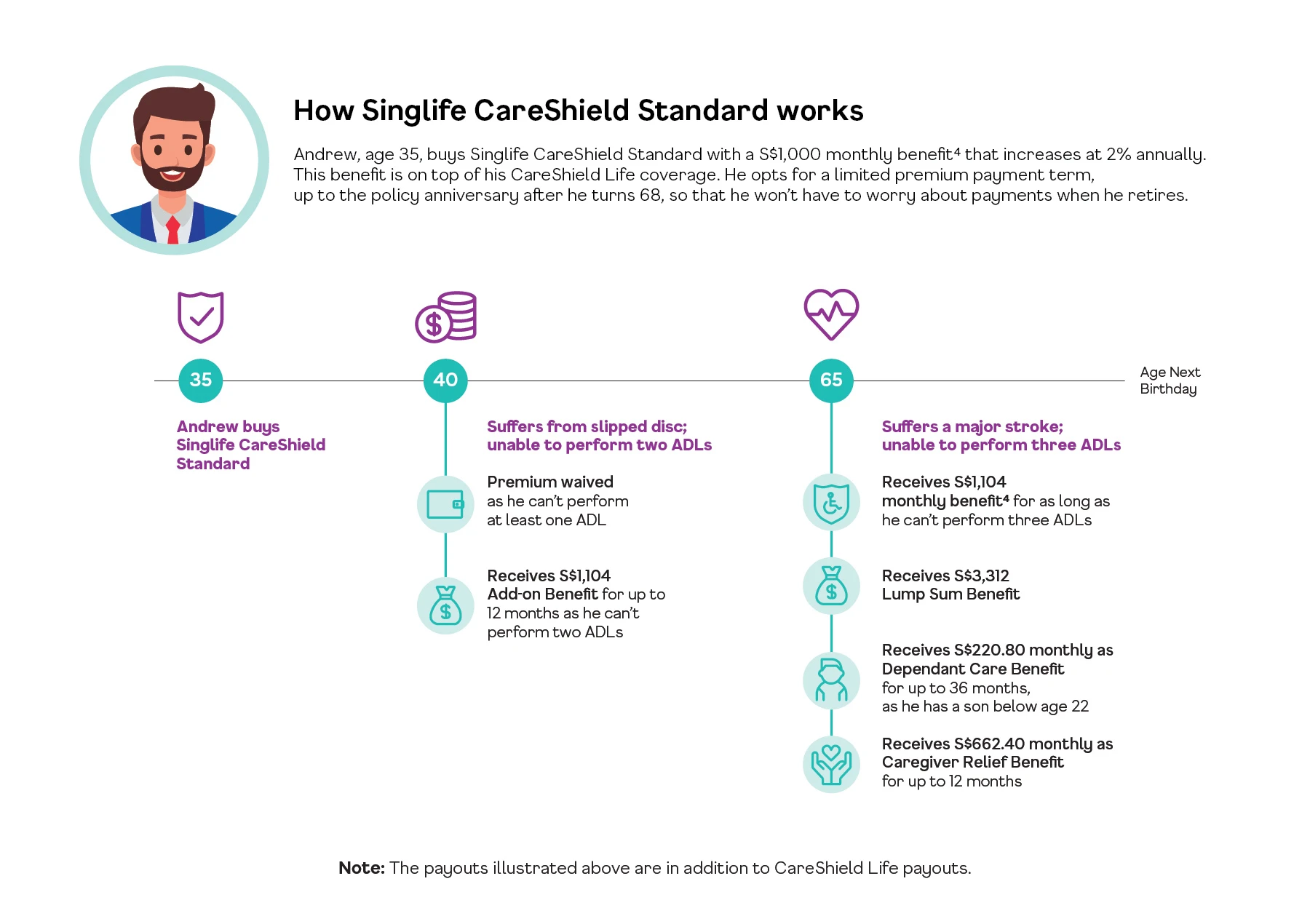

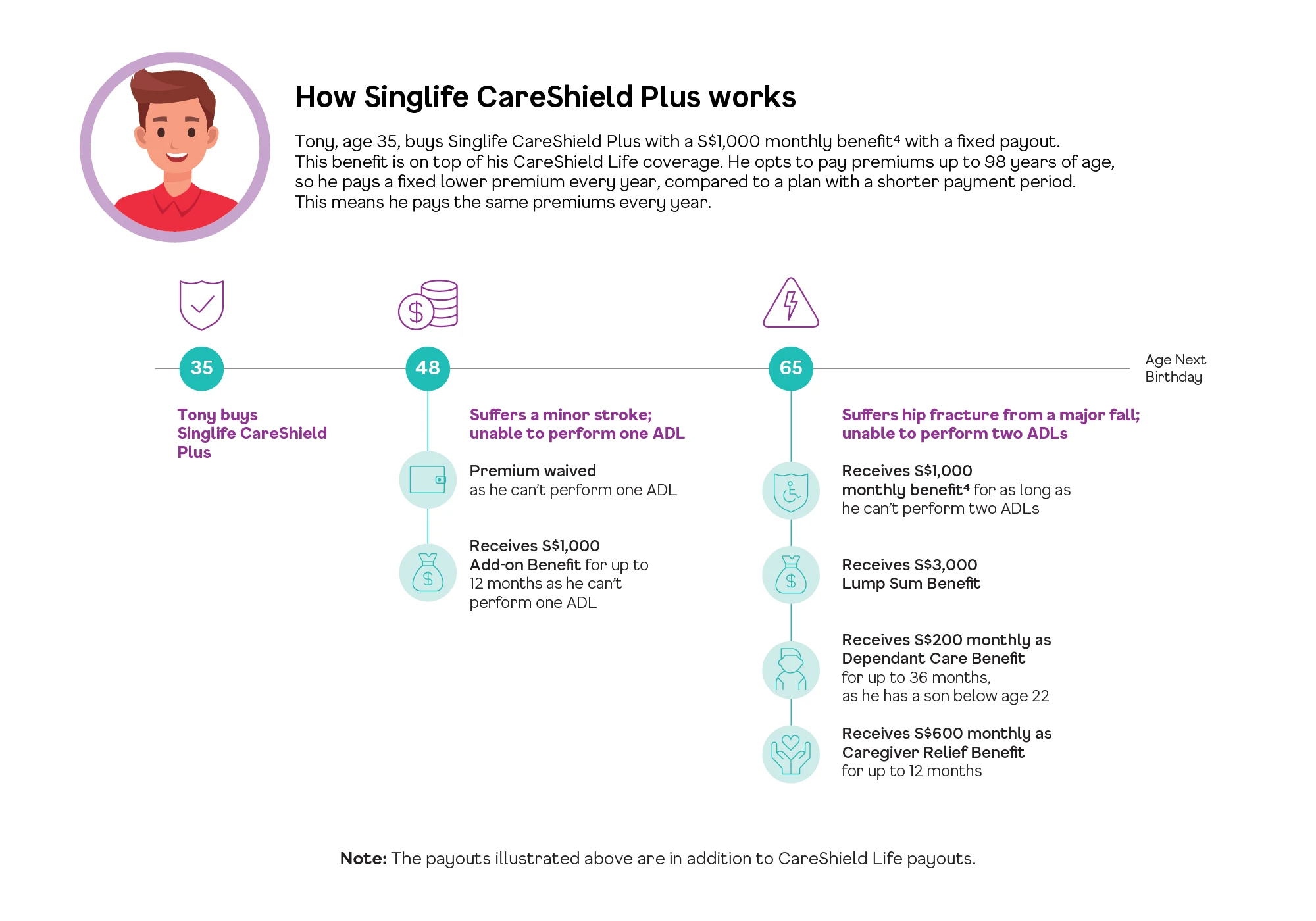

All ages mentioned refer to age next birthday (ANB).

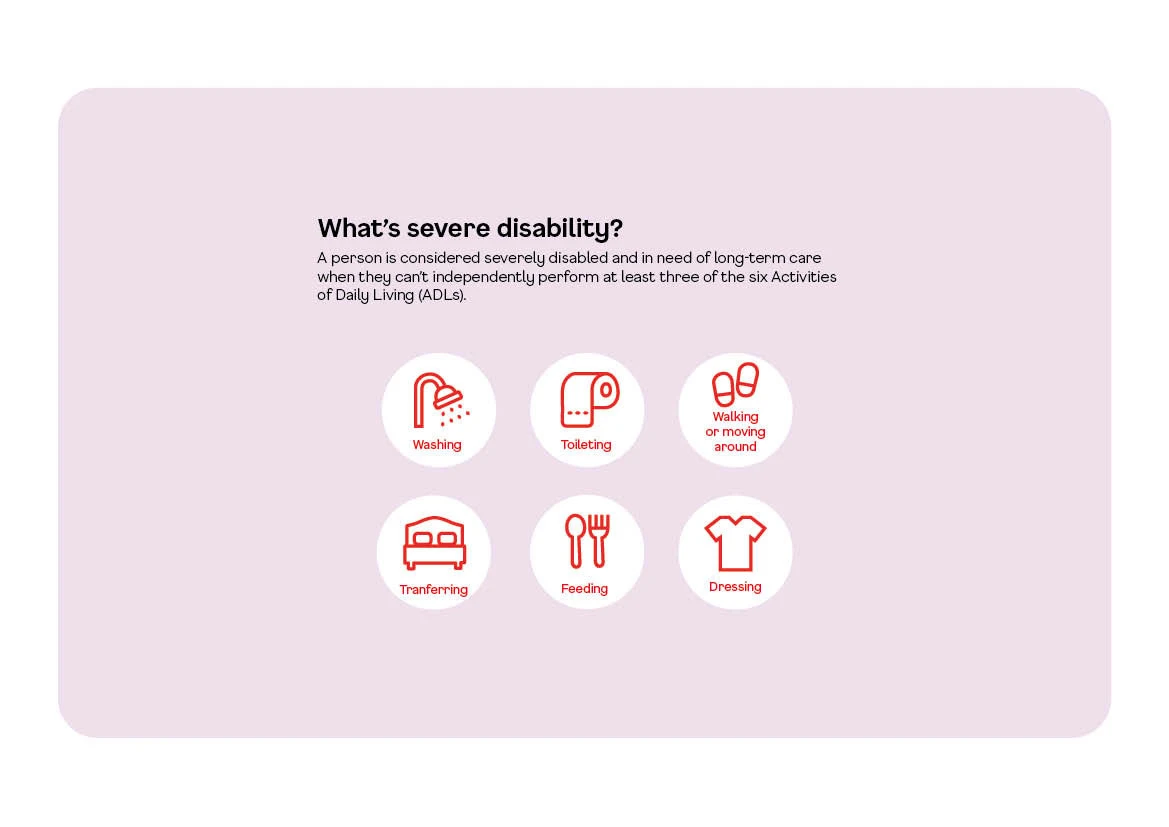

1. Severe disability refers to being unable to perform at least two (for Singlife CareShield Plus) or three (for Singlife CareShield Standard) of the six Activities of Daily Living (ADLs). The ADLs are washing, toileting, feeding, dressing, transferring and walking or moving around.

2. There are two ways to pay for a limited time; the later of the two options will apply. The two ways are:

a) The Life Assured may pay up to the policy anniversary after they turn 68

b) The Life Assured may pay for 20 years from entry age (if Life Assured joins at age 49 or older)

3. MediSave use is applicable to an amount of up to S$600, per calendar year, per life assured. Premiums exceeding this limit will have to be paid in cash. If there are insufficient funds in the designated MediSave account, cash payment will be required for the difference.

4. The monthly benefit refers to the monthly payout when the Life Assured suffers from a Severe Disability, as defined in the plan.

5. The Life Assured may receive an additional 20% of their monthly benefit – for up to 36 months – while they’re receiving their monthly benefit or rehabilitation benefit.

6. The Life Assured may receive an additional 60% of their monthly benefit – for up to 12 months – while they’re receiving their monthly benefit or rehabilitation benefit.

7. The policyholder may exercise this option, without providing further evidence of insurability at any of the following life stage events, when the Life Assured:

a) purchases a property;

b) marries, divorces or is widowed;

c) becomes a parent by having a newborn child or by adopting a child below 19 years old

d) salary increases by 50% or more from application;

e) completes a skills development course of at least six months;

f ) purchases a new individual life insurance policy or a Supplementary Benefit from us, with full underwriting at standard terms; or

g) spouse suffers a Severe Disability (with the inability to perform at least three of the six ADLs) or dies.

This option allows the policyholder to increase the policy’s monthly benefit with extra premium payable. The total monthly benefit that can be increased under this option is limited to 50% of the policy’s initial monthly benefit, as agreed at policy inception or at the date this option is exercised – whichever is lower. This option is extended to standard life only. Please refer to the Product Summary for more details.

8. The Deferment Period is a period of 90 days from the date the Life Assured is confirmed and certified by an Appointed Assessor as being severely disabled. The monthly benefit, Lump Sum Benefit, Dependant Care Benefit and Caregiver Relief Benefit will be paid after the Deferment Period. Waiver of Premium is applicable after the Deferment Period. The Deferment Period shall be waived if the Life Assured suffers from a Severe Disability that arises from the same cause, within 180 days from ceasing to suffer from the Severe Disability.

9. Payouts will be reviewed regularly and may be adjusted to account for claims experience and long-term changes in disability and longevity trends

10. A lump sum benefit will be payable if the Life Assured dies due to any accident or sickness while receiving either the Severe Disability Benefit or the Rehabilitation Benefit. The Death Benefit will amount to 3 times of the last paid Severe Disability Benefit or the Rehabilitation Benefit, whichever is applicable.

11. Add-on Benefit payouts start when you’re unable to perform 2 ADLs for Singlife CareShield Standard and 1 ADL for Singlife CareShield Plus